The Uneventful Foreclosure Crisis

The Uneventful Foreclosure Crisis

October 28th, 2015 - Every year in America $20-25 billion in real property taxes become significantly delinquent (>90 days).1 The total nationwide property tax base was just under $500 billion in 2014 according to U.S Census Bureau.2 Thus the national average property tax collections are 95% while the remaining 5% end up significantly past due. Local taxing authorities across the country use several methods to fill this gap, including: state funding, loans, tax sales, securitizations, and other financial instruments. Nearly every local government successfully funds their budget shortfalls each year through these methods.

Generally, only those municipalities with systemic blight, underfunded pensions, major population depletion problems (Detroit) or major cases of fraud and embezzlement (Jefferson County, AL) actually file for bankruptcy protection. Since 2010, nine local governments have sought such protection, and three were dismissed.3 That is a very small percentage when considering the 3,033 counties across the United States, and within those 19,492 municipal governments.4

Despite their ubiquitous use, these financing options for delinquent property taxes are unknown by most finance professionals and often mischaracterized in the media (see “Lacking Facts” below). Without interim financing, taxing authorities would be forced to be heavy handed on collections and quick to foreclose out of necessity. Payment plans, forbearance… forget about it - without some sort of immediate, massive cash inflow, none of those would be possible. Yet, the uneducated demonize any investor participation in such financing; they do so through anecdotal stories that are often absent of critical facts and full of sensationalism.

LACKING FACTS: The Washing Post’s three part expose on tax sales opens with a truly unfortunate story about an aging veteran struggling with dementia who lost his home to back property taxes. The article leads the reader to believe that he owed only $134 in taxes; however, it fails to reveal that the D.C. courts dragged out his case for four years in order to give him and his son time to raise money or sell his property in order to preserve his equity. The D.C. court held thirteen hearings regarding Mr. Coleman’s property, of which he attended only the three in the beginning of the case. During the case, Mr. Coleman neglected to pay his taxes over the next three years. The NTLA and numerous other organizations help property owners in this situation, but they or their family must pursue that help. The NTLA website has a list of government agencies and non-profit organizations that will assist persons in need with tax payment and legal work (www.ntla.org, under ‘Resources’).

Three years ago the National Consumer Law Center (NCLC) reported that property tax lien sales were ‘The Other Foreclosure Crisis’5, which forecasted a significant increase in American homes being lost to real estate tax foreclosures. They used statistics showing the increase in delinquent taxes during the credit crisis, but provided no hard evidence of increased household tax foreclosures. (Initial response to NTLA response here.) The National Tax Lien Association (NTLA) took on the challenges to discover the actual data, looking specifically at the thirty states, and the hundreds of municipalities within them, that allow investor financing of delinquent tax accounts. There exists no central reporting for this information; accordingly, the NTLA spent three years interviewing tax collectors, tax assessors, county clerks, and pouring over mounds of data to determine the true delinquent property tax rates and property tax foreclosure rates in America. The NTLA’s report is the most comprehensive and accurate data source for property tax delinquency.

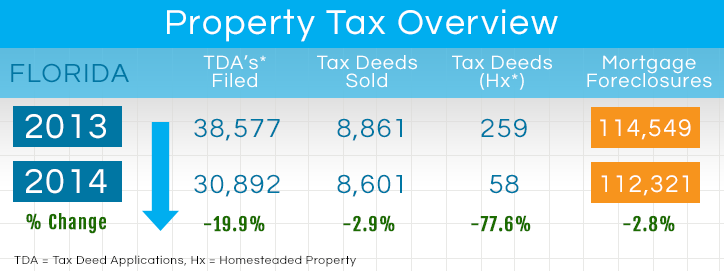

The NTLA discovered that the NCLC’s prediction was errant, it showed conclusively that the private financing of tax delinquencies works to preserve home ownership even better than the capital markets of the mortgage industry. Florida is a prime example in that it was one of the epicenters of mortgage foreclosures and because of its logjam in the courts it is still working through the backlog. If a large wave of property tax foreclosures was to hit any state, Florida would be the likely candidate.

Share on:

| |

Yet the data shows a significant downward trend in both tax liens and homestead tax foreclosures, with only 259 owner-occupied homes (notated with “Hx”) foreclosed in 2013, the year following the NCLC’s report. That number dropped to 58 the following year – a 78% decline. As compared to the mortgage foreclosures covering more than 110,000 properties each of those years with only a 2.8% decline between them. Likely, there was an increase in property tax foreclosures due to the great recession, but it was a far cry from a crisis itself. To the contrary, the data shows that private funding of the tax delinquencies gave the property owners (and lenders) time to get caught up without losing their homes. Tax liens have mandatory wait periods before foreclosures can begin, which provides significant time for property owners to reorganize their finances or sell the property themselves.

“The National Consumer Law Center predicted a tsunami of tax foreclosures and that Class 4 prediction turned out to be scattered clouds with no chance of rain,” commented Brad Westover, Executive Director of the National Tax Lien Association.

This is not to say that the entire NCLC report was errant; there were some good tips on notices to property owners and payment plans. All market participants want taxing authorities to employ best practices for ensuring delivery of notices and allowing payment plans. Given the puny volume of real estate that results from tax liens, it is clear that the investors are in the investment for the interest rate return.

“In my 37 years of public service as tax collector of St. Johns County, Florida, which includes America’s oldest city of St. Augustine, I have only had one tax foreclosure on an owner occupied property” stated Dennis Hollingsworth.

The NTLA research concludes that less than .05% of delinquent taxpayers ever lose their homes from non-payment of taxes. Tax sales allow homeowners more time to get back on their feet and settle their tax obligations to their local governments. Current taxpayers (95% nationally) are assured of paying only their fair share as they no longer are asked to cover the obligations of those not paying. These local governments receive reliable funds for vital services, including public schools, fire, police, public health and more.